The events of the last 18 months have dramatically accelerated the shift towards ESG. Covid-19 and racial and social justice protests have focused attention on social factors, while extreme temperatures, historic and catastrophic flooding and the administration change in the United States have galvanized action on environmental issues. Indeed, a host of stakeholders, including investors, insurers, regulatory bodies, asset managers, and corporate issuers, have all increasingly embraced environmental, social and governance (ESG) factors as part of their risk management framework.

It is undeniable that insurance has an environmental and social role to play in addressing the challenges caused by climate change. For example, in the last decade only 12 percent of economic losses in Asia were covered by insurance. In Latin America and Africa, virtually all losses were uninsured, leaving local populations dependent on federal or international financial support to aid in recovery.

Without insurance or social supports, the role of disaster risk financing becomes even more vital. Only 2% of crisis financing is pre-arranged despite many disasters, especially natural catastrophes, being foreseeable and predictable. This creates a cycle of disaster and aid, rather than reliable and timely post-disaster support. This is a poignant reminder of the importance of a Just Transition for developing economies and other vulnerable communities.

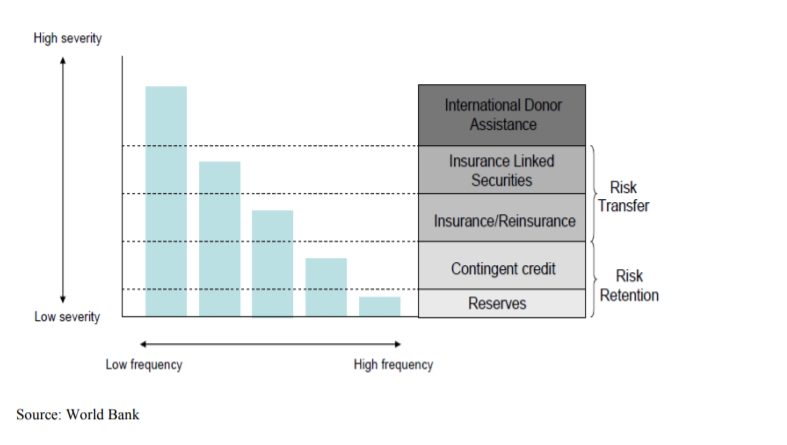

Instruments like catastrophe bonds (cat bonds), insurance-linked securities (ILS) and parametric coverage are just some of the tools that help bridge the coverage gap, providing much needed resilience to the local and global economy. In fact, in a 2014 World Bank working paper, it was concluded that the insurance sector had a key role to play in fostering inclusive economic growth. The paper concluded that “that the insurance sector contributes at a basic level to inclusive economic growth and the effectiveness of the credit function. It also shows that the latter impact may be particularly fundamental in assisting the poor to avoid poverty traps and to progress economically.” The paper went on to provide a potential framework for natural disaster relief funding (Figure 1), with ILS and insurance and reinsurance playing a major role for lower frequency, higher severity events.

Figure 1: Layering of ex ante and ex post catastrophe funding instruments

Against this backdrop, we have seen market participants, from insurers to investors to regulators, all increasingly focused on ESG generally, and on climate change mitigation and adaptation more specifically. Given the wide participation by a variety of stakeholders, we do not expect to see the focus on ESG and climate change abate any time soon.

The key drivers of ESG and climate change action within ILS and catastrophe bonds include:

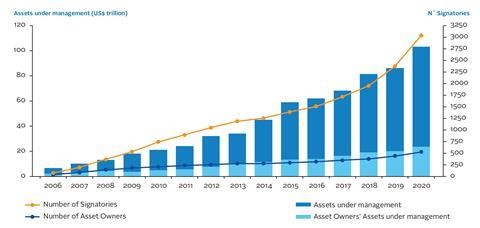

Investors: Surveys consistently show that ESG is increasingly important to institutional investors. For example, Natixis Asset Management found an 18% jump in institutional investors implementing ESG between their 2019 and 2021 surveys, with the totals growing from 61 percent to 72 percent. Aon’s soon-to-be-released 2021 Responsible Investment Survey found that, between 2019 and 2021, there has been a significant increase in dedicated responsible investment personnel, increasing from 5 percent to roughly 30 percent. In addition, the United Nations Principles for Responsible Investment (PRI) continued to see growth in asset owner signatories and assets under management.

Figure 1: Growth of Asset Owner Signatories to the UN PRI

Source: UNPRI

Source: UNPRI

Insurers: As natural catastrophes and weather-related events continue to make headlines, they are also bringing more attention to ESG at insurers. 2020 marked the sixth straight year with more than ten weather and climate events surpassing $1 billion in economic losses, according to CoreLogic . Aon’s own Weather, Climate & Catastrophe Insight report found that natural disasters caused $268 billion in global economic losses in 2020, $97 billion of which was insured . In the United States, where 76 percent of global losses were concentrated, the economic toll from natural disasters surged 28 percent above the average of the past decade. As a result of these and other ESG-related risks, ratings agencies like AM Best and DBRS Morningstar, among others, now evaluate how well or how poorly insurers incorporate ESG risk management. In addition, organizations like the Principles for Sustainable Insurance have attracted firms around the world who wish to formally embrace ESG. Efforts are currently underway to help insurers and reinsurers better understand their exposure to climate change, with the UN Principles for Sustainable Insurance piloting a project to use the Task Force for Climate Related Financial Disclosure (TCFD) as a framework for assessing this evolving risk.

The TCFD framework allows firms to focus on the environmental risks due to climate change by focusing on the following four pillars:

- Governance – how does the firm oversee and report on climate change risk?

- Strategy – how does the firm’s structure their risk management strategy to mitigate the physical and operational/transitional impacts of climate change, while also identifying business opportunities created in the transition?

- Risk management - how does the firm assess and manage climate change risks?

- Metrics and targets – what methodologies and data are behind disclosed statistics and metrics, and how does the organization plan to manage into a new climate-resilient paradigm?

Regulatory Bodies: More and more, regulatory bodies are homing in on environmental, social and governance issues. The PRI has identified more than 650 mandatory and voluntary ESG regulations and disclosure requirements globally and that number continues to grow. In addition, a wealth of disclosure requirements coming online in the UK and under discussion in the United States and Canada will compel firms to provide more transparency around ESG and climate change risks and opportunities.

Asset Managers: Earlier this year, we saw the implementation of the European Union’s Sustainable Finance Disclosure Regulation (SFDR), which included three classifications for investment funds to help prevent greenwashing.

- Article 6 funds do no integrate sustainability practices into their investment structure

- Article 8 funds are classified as “environmental and socially promoting”

- Article 9 funds target sustainable investments

Given the increased interest in ESG and sustainability from investors, these classifications could make it easier for investors to understand the sustainability of the funds in which they invest. We have already seen a few ILS funds achieve Article 8 fund classification status under the SFDR, showing the continued movement of insurance-linked securities and funds into the world of sustainability.

Corporate Issuers: Corporate issuers must increasingly disclose exposure to ESG risks through proxy statements, annual financial reports and sustainability reporting. In addition to keeping up with regulatory changes globally, this information influences scores from the roughly two dozen ESG ratings providers, which can influence everything from insurability to recruitment to access to finance.

Indeed, as climate change initiatives accelerate and global stakeholders look for ways to manage the volatility caused by global warming, ILS and cat bonds seem to have a natural role and we look forward to seeing how insurance and reinsurance can be part of the mitigation and adaptation equation going forward.

As firms navigate new forms of volatility such as climate change, Aon is committed to protecting and enriching the lives people across the world. At COP26, our goal is to mobilize private sector capital and drive collaboration with governments, academia, communities and businesses to deliver compelling solutions. Find out more about how we are tackling climate change at COP26.

About the Author

Paul Schultz is CEO of Aon Securities, Aon’s investment banking group. Prior to joining the company in 2000, he spent 15 years in the investment banking industry, and was head of Chase Securities’ Insurance Investment Banking Group, advising clients on M&A, leveraged finance, structured products and debt issuance.

Paul earned an M.B.A. from J.L. Kellogg Graduate School of Management and B.S. degrees in Electrical Engineering and Computer Science from Northwestern University. He is a Chartered Financial Analyst. Paul is also Treasurer of Northwestern University’s Public Issues Committee and also sits on Aon's Reinsurance Solutions' Executive Committee.