Ben Roe, Head of DC Consulting, and Jenny Swift, DC Market Specialist, explore priorities and trends from Aon’s 2024 Defined Contribution pension scheme survey

We are entering a new era for defined contribution (DC) pensions. Many young and mid-career employees will be entirely reliant on DC schemes to build a lifetime’s worth of pension savings.

With so much now riding on the quality of DC schemes, scrutiny of value for money, savings adequacy, strategy goals and good governance will increase from regulators and scheme members alike.

Aon’s 2024 DC survey, Five Steps to Better Workplace Pensions, surveyed 214 respondents from UK DC schemes of different sizes and from a range of industry sectors. We wanted to explore DC schemes’ priorities, their contribution structures, their approaches to investment, the focus on engagement and the nature of support for members at retirement.

Our participants represented the retirement savings of around one million DC savers, with combined assets of over £60 billon. Most were pensions directors or managers, HR, reward and benefits directors, or DC scheme trustees.

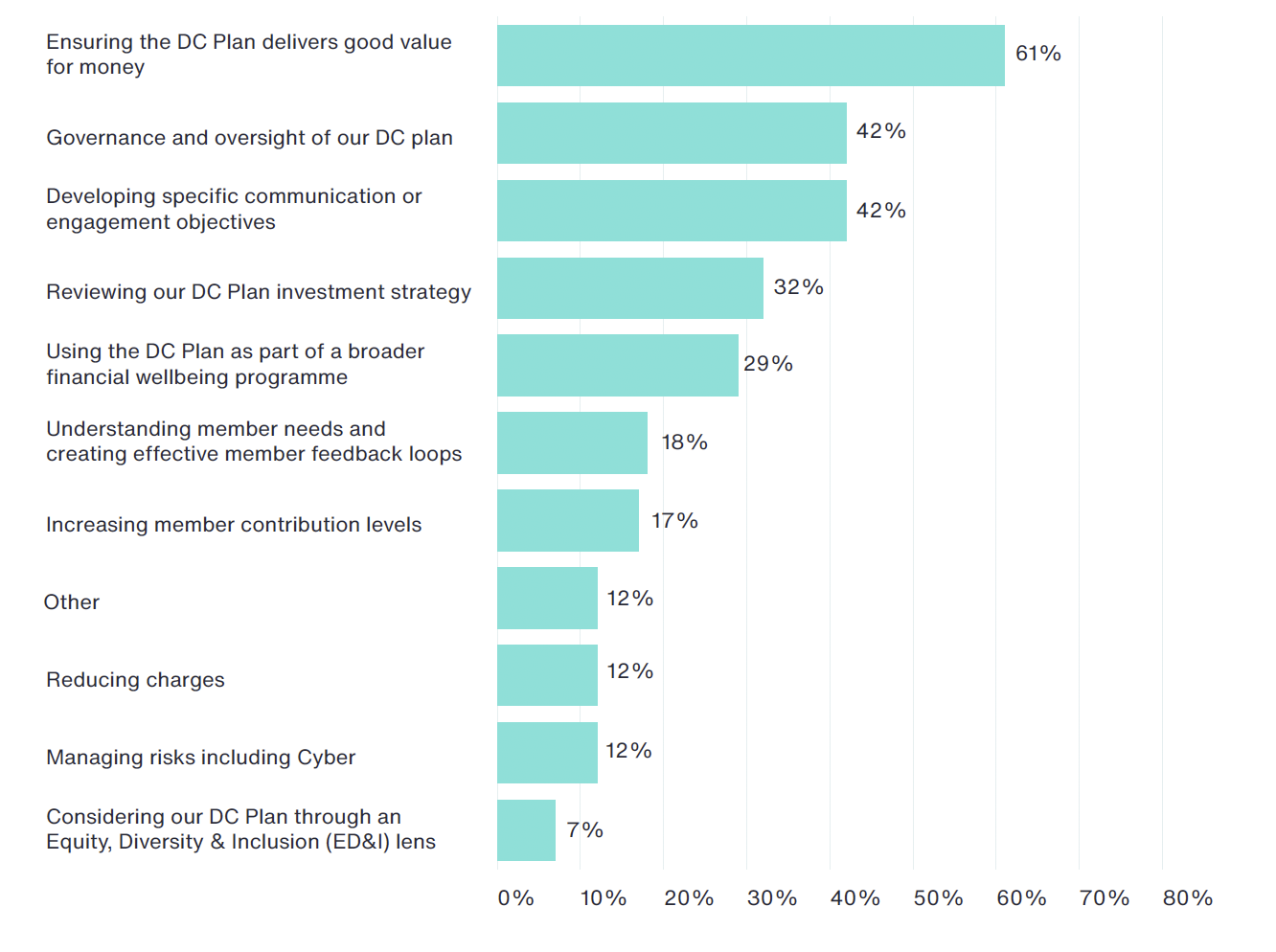

Value For Money: A Top Priority

Value for money should now be a key focus for any DC scheme. The Financial Conduct Authority (FCA) has released its proposed value for money framework for contract-based DC schemes, and legislation for trust-based schemes is expected in a future Pension Schemes Bill.

Crucially also, the chart below shows the impact that different elements of poor value can have on a member’s retirement outcome.

With that in mind, it is encouraging that 61 percent of survey participants said ensuring their DC scheme delivers good value for money is a top three priority. Other priorities such as developing communication or engagement objectives (42 percent) and reviewing the scheme’s investment strategy (32 percent), will also support the assessment of value for money against the FCA’s proposed framework.

Strategy Goals: More Focus Needed On Retirement Adequacy

Helping members to save for an appropriate standard of living in retirement is generally considered the main objective of a DC pension. However, our survey found that the top strategy driver is offering pension benefits in line with competitors (42 percent).

Only just over a third (36 percent) of respondents said providing a pension that delivers sufficient funds for employees to retire at a reasonable age was their main driver. Two years ago, when we ran our 2022 survey, that figure was 46 percent.

This feels like a step backwards. It increases the risk that pension strategies become disconnected from the savings needs of the workforce and that the pension scheme no longer acts as an attractive benefit to recruit and retain employees.

Governance: There Is Always More To Do For Scheme Members

Almost half (47 percent) of schemes want to change their current governance structure.

Master trusts are set to benefit from this, with 45 percent of respondents anticipating that they will be using a master trust by 2029, compared to 27 percent today. Only 26 percent of respondents anticipate that they will still be offering their own trust-based scheme by 2029, so there is a clear move away from single-employer trusts towards larger, outsourced structures.

The reasons for changing a governance structure vary, but almost a third (31percent) are switching because they expect the new structure to deliver better member outcomes.

For example, economies of scale could allow larger schemes to negotiate lower investment management charges, improving value for money as well as member outcomes. It may also mean they have access to a wider range of trustee expertise than some smaller schemes, to develop engagement approaches that improve adequacy – through higher contribution rates and smarter decision making.

Regardless of scheme governance structures, there is always more that schemes and employers can do for members. For example, there has been little change to average contribution rates since our 2022 DC scheme survey, despite growing recognition that employees are under-saving for retirement. And only 35 percent of schemes know what pension outcome a typical member might expect to have in retirement – again, showing little improvement from our 2022 findings.

Our 2024 survey shows that scheme managers can still do more to help members. Value for money measures will help decision-makers compare schemes and improve standards. It is good news that respondents are already focusing on those measures.

However, value for money is just part of the ultimate measure of DC success: members’ ability to save for an adequate retirement. That must remain at the core of all DC pension strategies.

You can download our 2024 DC Survey here: https://aon.io/3ySJLzh