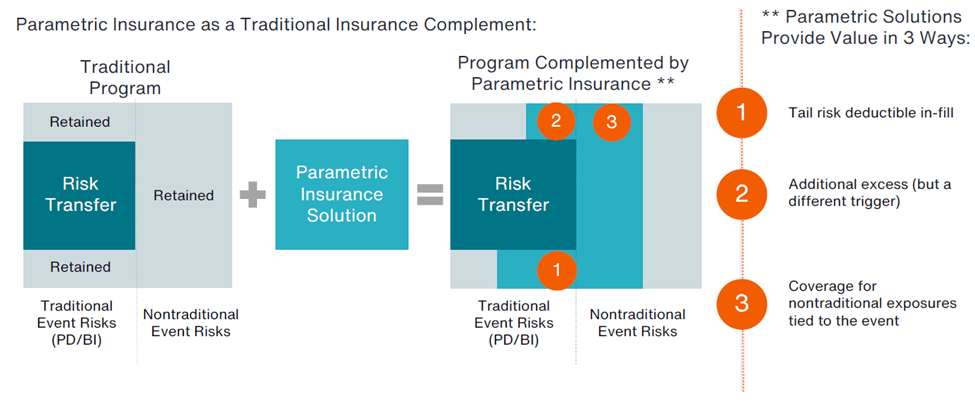

How Aon Has Implemented Effective Parametric Coverages Across Industries and Regions

1. Deploying Parametric Capacity as a Hurricane Risk Supplement in North America

An energy services firm on the Gulf Coast of the U.S. was concerned about the potential impact of a catastrophic hurricane on its facilities, especially following the effects of Hurricane Laura in 2020. The firm retained a substantial property risk with a $10 million deductible. Its existing insurance covers property damage only, with no coverage for business interruption and additional expenses.

Solution:

- The client’s traditional insurance program was augmented with a $50 million limit parametric solution triggered by a named storm track coming within 20 to 40 miles of the facility, as determined by the National Hurricane Center.

- Coverage attaches at a category three strength storm and increases incrementally its proximity narrows or intensity increases.

- The parametric solution covers any economic loss of the triggering event.

Evaluating the Outcome:

Parametric solutions provide a unique opportunity to assess exactly how a policy would perform if prior events were to reoccur. In this case, prior losses from Hurricane Laura yielded an uninsured exposure of $36 million. Had it been in place at the time, the parametric solution would have triggered a $37.5 million payout. The claim would be settled within a month of the event, providing liquidity at the time of the crisis rather than self-retaining or navigating a prolonged traditional claims process.

This type of “backcasting” analysis ensures parametric triggers are calibrated to potential economic exposures based on prior events.

2. Using Parametric to Help Maximize Resiliency to Earthquake Risk

A U.S. company’s campus is in an earthquake-prone area, exposing the client to a mix of controllable factors (engineering and construction of owned physical assets) and uncontrollable factors (resilience of employees, customers and other community stakeholders impacted by potential loss).

- The company was concerned about the long period without earthquakes the area was experiencing, which created questions about collective resilience and preparedness.

- Internal analysis pointed to significant concern around the resilience of local public utilities and services on which the company and its employees depend.

- Other concerns included challenges with traditional insurance, such as inherent coverage limitations, timing mismatch of claim payments vs. when the problem is managed, and a hard insurance market forcing large risk retentions.

Solution:

- In the design of the solution, the key challenge is to correlate the response to the exposure by defining key geographical areas of concern. Trigger locations associated with these areas are then set and become the building blocks for the parametric solution.

- Once measurement points are established, limits are distributed among each of the points in proportion to the level of exposure. For each trigger location, a pre-agreed payout matrix is created based on the intensity of exposure. This is determined by metrics provided by the U.S. Geographical Survey (USGS).

Evaluating the Outcome:

The solution can be tested based on past events or hypothetical modeled earthquake scenarios to assess the value and mechanics of the coverage. With this solution in place, the client maximizes its holistic capital response to earthquake exposure, maximizing “dry powder” and assuring its ability to navigate through volatility.

3. Addressing Severe Weather Risk with Parametric Solution in Asia

A leading renewable energy provider in the Philippines, with a vast network of physical infrastructure and distribution networks across the country, was concerned about the potential impact of a catastrophic weather event on its facilities. The Philippines averages 20 storms and typhoons annually, causing millions in losses and disrupting vital public utilities like electricity services.

The local Philippines insurance market provides very limited coverage via traditional property damage products for the energy transition and distribution industry. To address this, Aon needed to deliver a program to transfer key physical damage and business interruption exposures.

The business required a solution that would effectively price its risk exposure and simplify what had historically been a difficult and complex damage and insurance claims assessment process.

Solution:

- Aon modeled past catastrophic weather events over a two-year period, with a particular focus on windstorm/tsunami risk impact.

- A bespoke “pole and wire” windstorm model was developed to quantify the infrastructure and property loss at different pre-agreed levels of maximum sustained wind values on a one to five category scale based on historical pricing. This allowed us to develop an appropriate cost for potential damages to the network.

- The captive obtained terms for a parametric solution covering windstorm risk, with claim payments designed to match storm proximity and severity.

Evaluating the Outcome:

The solution enabled the energy company to make quicker and more straightforward claims. In December 2021, the program was triggered following Typhoon Rai, with a payment made within 30 days (and within ten days of the program being finalized).

The most significant aspect of the solution has been eliminating the difficult, time-consuming and complicated damage assessment work that was previously required for a claim on a traditional insurance program.

Talk with Us

If you would like to discuss if parametric coverage is right for your organization, please do not hesitate to get in contact with our team.

North America

Michael Gruetzmacher

Head of Alternative Risk Transfer and Innovation

Aon Commercial Risk Solutions, North America

[email protected]

Asia Pacific

Benjamin Miliauskas

Treaty Broker

Australia and New Zealand Reinsurance Solutions

[email protected]

Alex Davies

Director

Construction, Power & Infrastructure, Asia

[email protected]