National Pension System: Market Pulse

Chitra Jayasimha

FIA, FIAI, Actuary and Practice Leader,

Retirement and Investment,

Aon Hewitt

Vishal Grover

Senior Consultant, Retirement and

Financial Management Practice,

Aon Hewitt

Siddharth Saxena

Consultant,

Retirement and Investment,

Aon Hewitt

It has been more than three years since the government

opened the National Pension System (NPS) to the

corporate sector, with the intent of transforming India

from an almost pension-less society to a pensioned

society. As a pure and real pension scheme offered by the

government, NPS has attracted a fair bit of attention.

What is it? NPS in Short

NPS is a defined contribution style superannuation scheme

launched by the government, originally for government

employees in 2004 and subsequently extended to the

citizens of India in 2009 and to the corporate sector

in 2012. Within the corporate sector model, both the

employer and the employee may contribute to the

employee’s NPS account. The contributions made, along

with the returns, will be available to the employee upon

retirement for a combination of options including part

commutation and purchase of annuities.

Up to 10% of the basic salary per annum can be

contributed by the employer on behalf of the employee

and the entire contribution does not attract tax in the hands

of the employee. The same contribution by the employer

is also allowed as a business expense. Additionally, an

employee's own contribution is eligible for tax deduction

for up to 10% of the basic salary, with an overall ceiling

of `1.50 lacs under Sec. 80 CCE of the Income Tax Act.

From FY2015-16, an employee will also be allowed a

tax deduction in addition to the deduction allowed under

Sec. 80CCD(1) for additional contribution to his/her NPS

account, subject to a maximum of `50,000/- under Sec.

80CCD 1(B). As such, effective tax benefits on investments

has increased to `2.00 lacs from the current financial year.

In addition to the attractive tax benefits for both the

employer and employee, the NPS also scores in other key

parameters. These include:

- High portability with a unique NPS account number

provided to each employee, which allows for easy

transferability during change in employment

- High flexibility in terms of choice of fund managers

and asset classes

- Exposure to market and equity linked returns

- Regulated by the statutory body – The Pension Fund

Regulatory and Development Authority (PFRDA)

- NPS is one of the lowest costing pension schemes in

the world in terms of fund management and

administrative charges

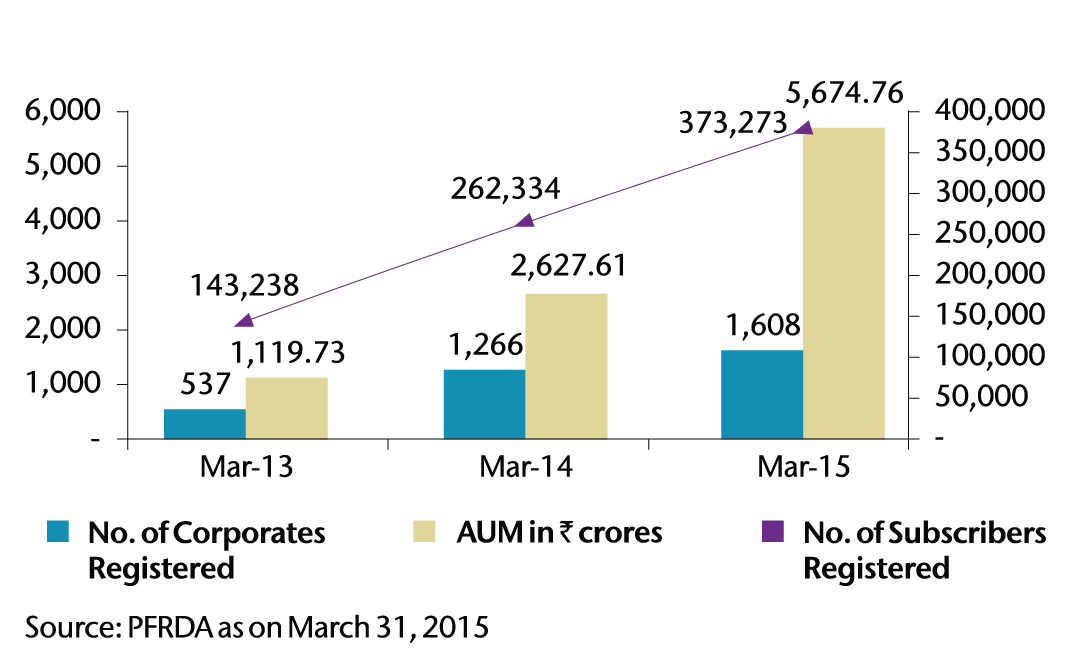

Market Prevalence

As seen alongside, the NPS corporate registrations and

assets under the management have been showing healthy

growth rates over the last few years. As on March 31, 2015,

3,73,273 corporate employees were covered under the NPS.

However, it should be noted that while more than

1,600 corporates have registered under the scheme, not

all may have started contributing on behalf of their

employees.

If we also include government employees and private

individuals, the total member subscriptions would stand

at 87,48,649 and the total assets under management

would be `80,855 crores as on March 31, 2015.

Aon Hewitt NPS Benefits Survey 2015

Aon Hewitt conducted a market pulse study to draw

insights and feedback from corporate employers, both

subscribers and non-subscribers to NPS.

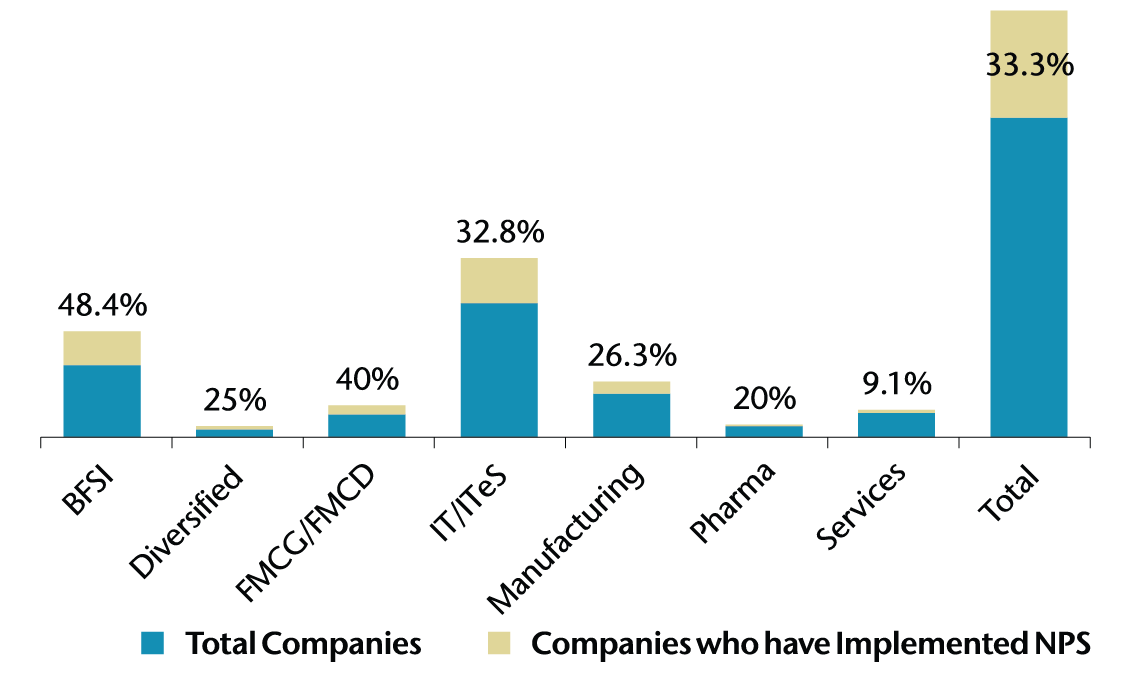

There were a total of 138 companies who participated

in the survey, with maximum participation from BFSI and

IT/ITeS sectors.

Approximately 33% of the survey respondents were

enrolled for NPS, with BFSI and FMCG/FMCD companies

driving this number.

In terms of the implementation strategy adopted by

employers, the key insights drawn from the survey are:

- Two-thirds of the companies who have enrolled for NPS

have offered the benefit to all their employees

- The majority of subscribing companies have included

the NPS benefit as a part of their flexible compensation

structure, where an employee can choose whether or

not to opt for this benefit

|