National Pension System: Market Pulse

-

Most organizations prefer to appoint Points of

Presence (administrators), which are banks with

whom the organizations have their salary or

corporate accounts. The key expectations from POPs

include professional service levels, quick resolution

Employees and Communication

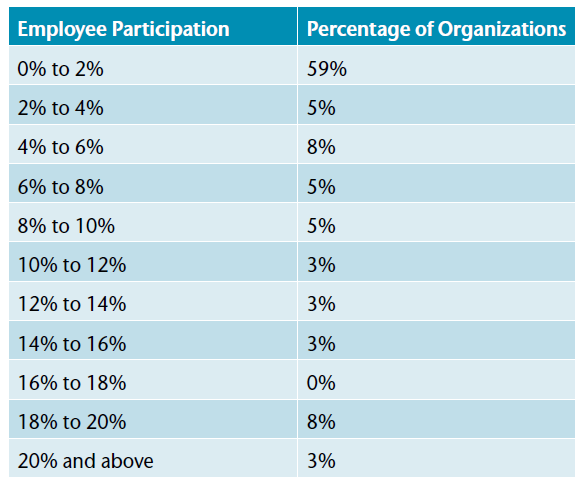

One disturbing trend observed from the survey results is

the dismal participation/enrollment of employees in the

NPS scheme. Only 20% of the organizations that have

implemented the NPS have achieved employee

subscription of 10% and above.

An employer may have taken the first right step in

setting up the NPS benefit for his/her employees, but

the responsibilities continue beyond merely introducing

the scheme. The fact that the NPS is voluntary and the

employees can choose not to enroll for it makes it critical

for employers to have an active and smart communication

and awareness strategy around NPS. It is a clear challenge

for employers to educate their employees to the point

that they can make an informed decision about the

scheme, especially for the younger generation who is

openly inclined towards cash in hand. The strategy has

to be set using the latest communication tools and has

to be done on an ongoing basis in order to achieve a

better rate of participation. This strategy may include:

- Wider awareness around lack of retirement savings and

the eroding power of inflation in India

- Use of retirement and savings calculators to demonstrate

ideal Net Replacement Ratios post retirement

The modes of communication could be regular emails,

posts on the intranet, presentations, social media

campaigns, workshops, etc.

-

Having a different strategy for blue and white collar staff

Employers should also be careful not to hard sell the NPS,

and the communications should be more holistic in nature.

It should be made sufficiently clear to employees that

returns from NPS are market-linked and that there is a

chance that employees' expectations may not be met.

Conclusion

The concept of a strong, universal social security system

has never existed in India. The primary reason for this has

been the fact that India has been a developing country

with the world's second largest population to support.

As such, historically, governments have always relied on

individual savings and employer sponsored plans to meet

the retirement and social security needs of the population.

It is still early days for the NPS, and it remains to be seen

if this scheme can achieve the mass appeal and scale

within the retirement savings landscape that has been

achieved by the decades old Employees Provident Fund.

|