Leveraged Life Insurance for Business Owners and HNW Individuals

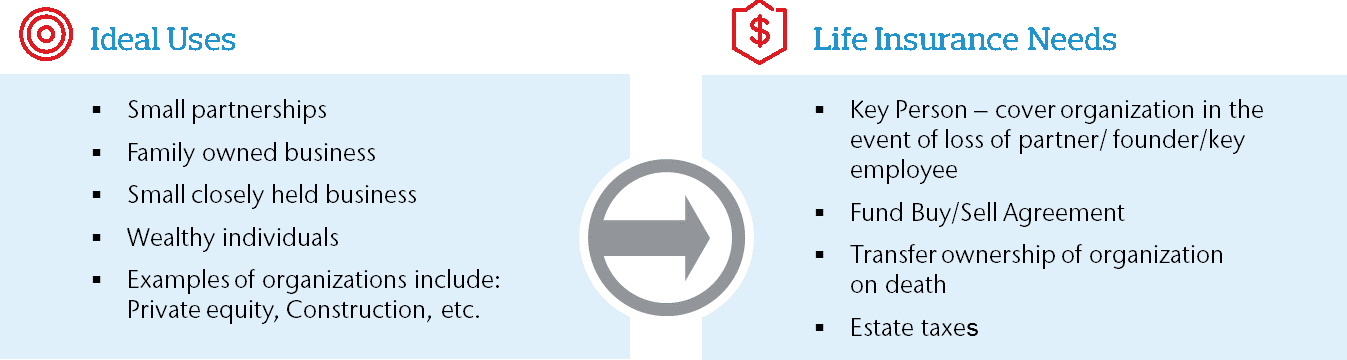

Organizations and wealthy individuals need life insurance for a variety of reasons, examples include:

Let’s look at the traditional way insurance is purchased.

Businesses often purchase low cost “term” insurance which provides temporary protection. If the insured outlives the term, the insurance expires without value.

Example: $20M of Coverage, 50 Year Old1

| Type of Coverage |

Initial Death Benefit |

Premium Structure |

Annual Cash Outlay |

Cash Outlay Through Year 20 |

Cash Value at Age 85 |

Death Benefit at Age 85 |

| 20 Year Term |

$20M |

20 Year Level |

$40.7K |

$815K |

None (lapsed) |

None (lapsed) |

Permanent cash value insurance offers an investment element and coverage through life expectancy. This type of insurance is more expensive and ties up significant amounts of cash.

Traditional

Whole Life1 |

$20M |

20 Year Level |

$430K |

$8.6M |

$14.5M |

$20M |

Aon’s Approach

Utilizing our vast insurance and banking networks, Aon has created a strategy that allows clients to obtain permanent life coverage for the same cost as term.

Leveraged

IUL2 |

$25M |

Interest for 20 Years |

$40.7K |

$815K |

$14.7M |

$30M |

1Assumes 50-year-old in preferred health, non-tobacco user.

2Assumes 7.45% crediting, 2.75% loan yr. 1; 3.25% years 2–10 (capped), 4.5% thereafter. Loan repaid in year 21.

Program Advantages

The program works by borrowing premiums from a preferred lender and repaying the bank from policy cash values at a later date. The policyowner owns all cash value that remains after the bank is repaid. This approach has the following advantages:

- Minimal cash commitment, typically about the same cost as a term policy

- All premiums accumulate long-term value (unlike term premiums which are never recovered)

- Ability to lock in borrowing rate caps (currently between 2–3% April 2020)

- Policy gains entirely avoid taxation (no tax on gains, no tax death proceeds)

- Downside market protection (if market is up, you participate; if market is down, no loss)

Why Now?

- Low Rates. The Fed is slashing interest rates, meaning the borrowing rates are historically low which translates into lower cost to you. You can lock in rate caps for up to 10 years.

- Downside Market Protection. These products include downside market protection. With all the market turmoil in response to COVID-19, this asset gives you protection when the market is down; and when the market recovers, you participate in equity returns.

We’re here to empower results.

To learn more about Leveraged Life Insurance solutions, please contact us