Brexit Update: Insurance contract continuity

With an ever-changing political scene and limited time left to conclude the negotiations for the United Kingdom’s (UK) exit from the European Union (EU), attention is now beginning to turn to the potential consequences of Brexit. This article covers the issues that insurers face and considers the interplay between insurers’ contractual obligation to continue to service policies (including paying claims) versus the practical impact that local regulation might have on their ability to do so.

Brexit means Brexit

Despite European leaders reportedly saying that it is not too late for the UK to remain in the EU, the UK Government remains steadfast in its course to deliver on the result of the UK’s 2016 referendum. The UK’s latest plan is clear that after 29 March 2019 (or an anticipated later, post-transitional date) the UK will leave the EU, will rescind its membership of the Single Market and the EU Customs Union and will no longer be bound by the EU’s ‘Four Freedoms’ – the free movement of goods, capital, services, and people. According to the UK Government, ‘Brexit’ will happen.

The EU’s Single Market

The current EU membership has allowed the UK to operate within the EU’s Single Market, providing it with a relatively frictionless route for trade anywhere within the European Economic Area (EEA), whilst also eliminating inter-EEA tariffs, quotas, and taxes on trade, and according to the European Commission's website, generally removing regulations to allow unrestricted movement of goods and services. As part of this Single Market regime, insurers currently enjoy the same freedom. The freedom to operate in any member state regardless of country of domicile, under so-called ‘passporting rights’, which give insurers who are regulated in their own EEA country, access into any other EEA member country without needing to be separately authorised in it.

Exit negotiations

As the UK and EU now enter the final stages of negotiating a formal Withdrawal Agreement, UK Government has set out its own aims in a white paper, titled The Future Relationship between the United Kingdom and the European Union. Controversially, the paper offers very little comfort for the Financial Services sector. For example, it seems certain that insurers will ultimately lose passporting rights, yet it does not offer an obvious alternative trading solution to mitigate the impact of such loss. As a result, insurers are afforded no clarity on whether they may be able to continue to service existing cross-border business following Brexit.

Several alternative trading regimes have been suggested, the most favoured being ‘Solvency II equivalence’, whereby the UK’s rules and regulations are recognised by the EU as equivalent, or sufficiently similar, to those contained in Solvency II to facilitate aspects of EEA-UK trading. But such alternatives are not without their problems. In particular, ‘equivalence’ can easily be revoked with only 30 days’ notice. This leaves commentators to surmise that the UK would need a detailed agreement for any alternative arrangement to work. And as this would take both time to negotiate and a willingness on the EU’s part to talk, these alternatives do not appear to be immediate, viable options.

So, it seems that affected insurers will need to find their own solutions to this dilemma. Brexit not only potentially reduces future market choice and capacity, but may also give rise to regulatory concerns for insurers with current and past policies covering cross-border EEA risks (unless they change their operating models or have / or obtain separate licenses). Furthermore, without such a change, not only could insurers be prevented from writing new cross-border insurances but they could also face regulatory censure by meeting their contractual obligations to service such policies post-Brexit under both existing policies and for past liabilities on expired policies. In particular, the payment of claims by the insurer may cause it to act in breach of local regulation. As Nicky Morgan, Chair of the House of Commons Treasury Select Committee put it, if the issue is not resolved, insurers may have to choose ‘to break the contract or break the law’’ (letter to the Chancellor of the Exchequer 14 Sept ’17).

What policies or insurers are affected?

Not every insurance policy will be affected by Brexit and the consequential loss of passporting rights.

Importantly, some insurers already have authorisation in both the UK and elsewhere in the EU, which may allow them to continue largely unaffected post Brexit. Otherwise, affected insurers are expected to retain the ability to write certain cross-border UK-EEA risks (e.g. marine, aviation and transit policies) under the World Trade Organisation’s General Agreement on Trade in Services (GATS) provided that these classes are within the insurer's host state's GATS Specific Commitments and any requirements of its host regulator are met, which may well include a requirement for local authorisation. This does however, also depend on the UK’s ability to obtain WTO membership in its own right, including participation in any agreements to which it is currently a party by virtue of its membership of the EU.

Whether other ‘non-admitted’ insurances (i.e. insurances written by an insurer that is not authorised to do business in the country where the risk is located) are allowed, will depend on the specific rules adopted by each of the individual countries. For example, Aon understands that currently France and Italy do not allow unauthorised insurers to carry out regulated insurance activities nor allow buyers to procure non-admitted insurance, whilst Germany does allow for non-admitted insurances (except for compulsory classes) if certain conditions are met. However, even this is not a guaranteed position, because recent indications are that regulators in some EU member states are looking to tighten the rules for non-admitted business. This follows a 2015 comment by the EU Commission expressing the view that insurers ought only to provide insurance in countries where the insurer is locally authorised.

So far as insurer authorisations are concerned, it is not always immediately obvious which insurers operate under passporting rights, whether this is an EU insurer trading in the UK or a UK insurer trading in the EU. Either way, insurers looking to write cross-border risks between the UK and EEA are likely to encounter the problems outlined above. There is one known exception, in that the UK Government has already intimated that it will temporarily continue to permit EU insurers to operate within the scope of their current permissions after Brexit while seeking UK authorisation. They will therefore be able to write new business and service existing business, including the payment of claims to UK-based clients for the period of this permission. However, the EU authorities have not yet given the same assurances, and so, as it stands, UK insurers may not be permitted to pay claims to, or otherwise service, EU-based clients.

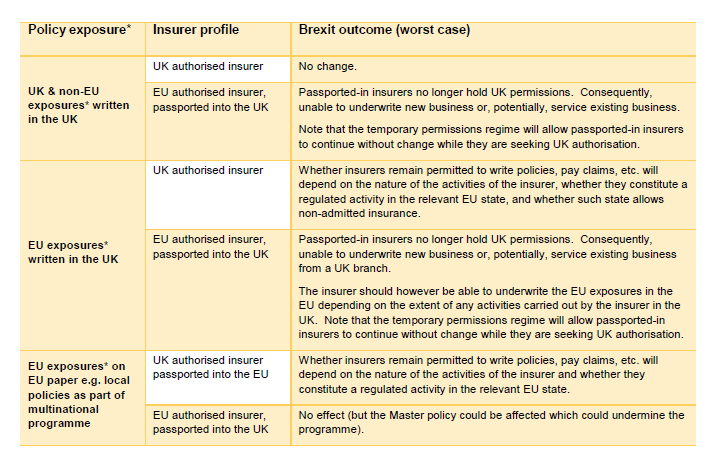

The possible effect of Brexit on insurance policies

The following summarises some of the potential impacts of Brexit on insurance business. What is not commented on here, is whether there are any additional EU tax implications that result because of Brexit.

*Solvency II sets out the basic rules on determining the location of risk, although these may be subject to local law interpretation. Solvency II provides that buildings and contents cover will be determined by the location of the property, vehicle cover is determined by the state of registration, short term holiday cover is determined by the location where the policyholder took out that cover, and all other policies will be determined by place of residence/establishment of the policyholder.

Insurer response

Most insurers have been working on their Brexit plans for some time. These have largely considered the worst-case scenario of a no-deal Brexit (which has increasingly looked like a real possibility as we move closer to the Brexit date without a clear view as to the future relationship between the EU and the UK).

Insurers are implementing changes to alleviate their own potential problems and reflect the peculiarities of their business. For example, several insurers have or are in the process of restructuring their businesses, relocating, re-registering and opening new operations in other EU member locations. For each of these options, there is a costly and often time-consuming process of obtaining all the necessary authorisations.

Mostly such actions are intended to give insurers the ongoing access to the EEA or UK which should allow them the freedom to continue to trade post-Brexit. However, it does not categorically nor automatically solve the potential problem regarding honouring their existing obligations under both current Both brokers and insurers lobbied the Government early about the need for a transition period after the Brexit date, during which the status quo can be maintained. And whilst the UK and the EU have agreed this in principle to expire 31 December 2020, it can only happen if agreement is reached on the whole Withdrawal Agreement by mid-October 2018. Without such transition period, the fear is that some insurers will simply not be ready – and regulatory requirements will not have been completed, which could expose insurers to regulatory censure in continuing to trade and pay claims post-Brexit.

What happens next?

We cannot yet say that the insurance industry is totally Brexit-safe, but insurers are working very hard to adapt to the probable post-Brexit world.

Aon will continue to keep close to both the political situation and insurers’ evolving positions. We are working to try and ensure, as far as we can, that policies and programmes are safeguarded and that there is as little disturbance to clients as possible. However, there is no “one size fits all” set of solutions and unfortunately no simple endorsement that will guarantee cover post-Brexit.

Within the confines of this paper, it is not possible to delve into the specifics of how any particular programme may operate post-Brexit, but please contact your usual advisor for more information and updates about how Brexit might impact your own insurance programme. and past policies. Usually this can only be overcome for sure by insurers completing a formal Part VII transfer (or the local law equivalent). This is a court sanctioned, legal transfer, which in the UK is governed by Part VII of the Financial Services and Markets Act 2000 and is often a lengthy, complicated and time-consuming process. It therefore remains to be seen whether all such transfers will be implemented by the Brexit date.

Please speak to your client management team about implications to your current risk transfer polices.