A Workplace Risk Hiding in Plain Sight: Addressing Financial Diversity

By Head of Financial Wellbeing, Paul Gordon

While most organisations have processes and frameworks in place to manage workplace diversity, there remains a significant, frequently overlooked risk that can have deep and widespread consequences if not properly understood: financial diversity.

It is often assumed that people on lower salaries are more affected by financial stress, but we have seen it doesn’t discriminate; everyone, from the junior levels to the CEO, can struggle to meet their commitments, especially when economic conditions are challenging. For example, research tells us more than a third of Australians who earn six figures are living pay day to pay day, with less than a month’s worth of their salary saved1. Understanding financial diversity is key to providing effective support.

New Challenges Faced by The Modern Workforce

Financial wellbeing used to be discussed in terms of creating wealth, managing debt and having sufficient retirement savings. However, now we approach it at a much more fundamental level: the ability to get through current financial conditions without harmful stress.

In the Asia Pacific region, employees are grappling with several significant challenges that directly impact their financial wellbeing.

Rising Cost of Living

The rising cost of living is a pressing concern in many countries in the region.

In Australia rising inflation has seen the cost-of-living surge. Australia has experienced 14 interest rate rises since 2022. People under 45 have never encountered challenges such as these; 1990 was the last time inflation was above 7%2 . In the current economic climate,1 in 4 Australians are finding it hard to get by on their current income.3

Meanwhile, India has seen inflation rates fluctuate between 4.5% and 7.5% in the past year. Hong Kong and Singapore have only increased their reputations as costly places to call home – Hong Kong is now the most expensive city to live in the world4 , while Singapore’s CPI increased by 4.8% in 2023, following a 6.1% rise in 2022. In the Philippines, economic strain is being exacerbated by rapid population growth, currently at a rate of 1.53%, with a population density of 399 people per square kilometer. Factors such as high birth rates, urbanisation, and labour migration drive this growth, putting additional pressure on resources and infrastructure.5 Only China has avoided rising cost of living concerns, with a slow down in CPI; cost of food dropped by 0.3%.

Housing Affordability

Housing costs have skyrocketed in many APAC cities, putting home ownership out of reach for a large portion of the workforce. Even renting can consume a significant portion of an individual's income, leaving little room for savings or discretionary spending. This lack of affordable housing options can lead to long commutes, reduced quality of life, and increased financial pressure.

Across cities in India, a housing shortage and higher interest rates have contributed to an annual average rise in house prices of 15% for the past five years. Hong Kong remains the world’s most unaffordable property market for the fourteenth year straight, with the average home in the city costing as much as what the average household income would earn in 16.7 years.6 In Singapore, renters have faced a 55% rise in rents between 2020 and 2023. The Philippines’ rapid urbanisation and economic challenges have led to a substantial housing backlog, which was estimated at 6.5 million units in 2022 and projected to rise to 22 million by 2040.7

In China have housing prices dropped: according to CEIC data, China’s housing index has dropped to 134.277 in the end of 2023 (using 2010 as 100 mark), and further down to 131.522 in the first quarter of 2024, a trend that is expected to continue.

Job Security

In an era of rapid technological advancements and economic uncertainty, job security is a major concern for employees. The fear of job loss or being unable to find new employment can create a sense of instability and financial insecurity.

This is of particular concern among the younger generation in India, who are struggling to find employment: approximately 7-8 million young people are being added to the labour force each year, with youth accounting for almost 83% of India’s unemployed workforce.8 Top firms in the IT sector, one of the biggest job creating sectors for the youth in India, cut their workforce by over 72,000.9 In Hong Kong, it’s the financial services sector feeling the pain, as several companies report layoffs attributed to less deals and stock market hitting record lows at the start of 2024.10 Singapore, with its competitive job market, remains strong on the job creation front with the highest number of newly created jobs in five years, and a low average rate of unemployment of 1.9%.11 The United Nations Development Program (UNDP) highlights that the Philippines faces significant challenges in sustaining economic growth and human development due to the high risk of job loss and displacement from frequent natural disasters and climate-related events.12 Moreover, a survey by Ipsos revealed that a significant portion of Filipinos, about 73%, fear that AI will lead to considerable job losses, which is higher than the global average.13

Delivering on Financial Wellbeing

Now more than ever it is important to help employees tap into their behaviours around how they deal with money and identify habits that could be adjusted to make a difference.

Add to this the expectation for managers to be better equipped to support employees in the wake of COVID, and the need for an effective financial wellbeing strategy may be evident.

Within the contract between an employer and an employee, remuneration plays a significant role. Yet some managers may be apprehensive talking to an employee about their financial wellbeing. Conversations that feature remuneration, incentives or bonuses, or benefits are just a few of the many opportunities for a general, non-invasive conversation to assess the financial pressures that may be influencing an employee’s behaviour and intentions.

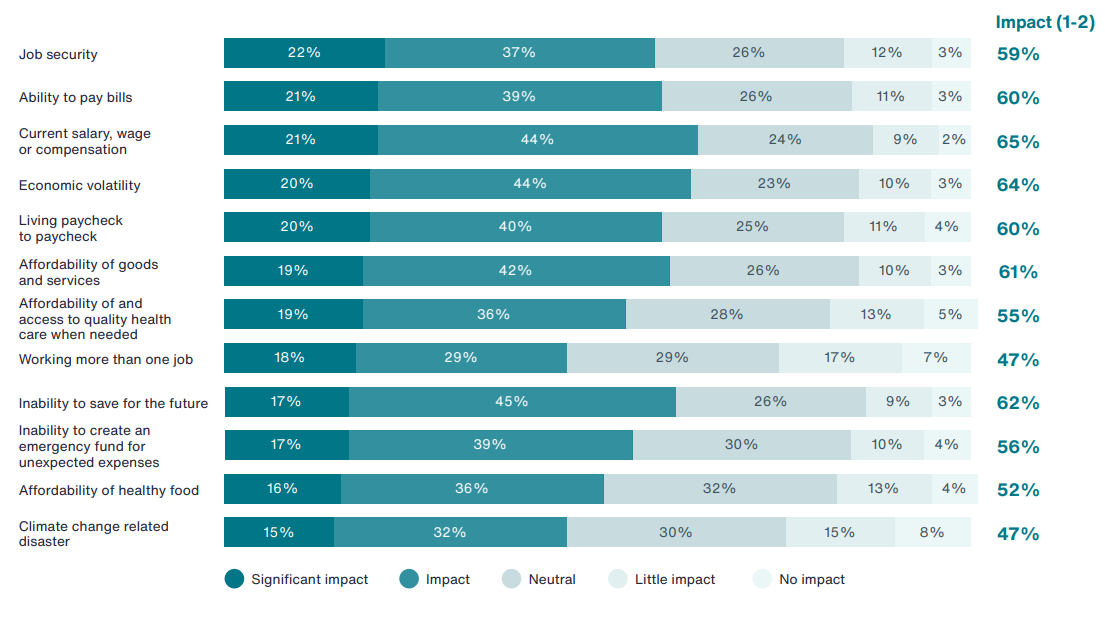

Financial Stressors Impact on Workforce14

Understanding the diversity within your workforce of behaviours towards money is helpful to being able to provide effective assistance. Aon uses a behavioural framework where people place themselves in a certain category after reflecting on their money habits. It is not a matter of one category being better than the others; it is more about gaining an awareness and understanding of attitudes to money that could help improve financial behaviours and potentially reduce stress, but also may help increase productivity and minimise flight risk.

What are the Risks of Ignoring Financial Wellbeing?

Many employees across the Asia Pacific region are finding it hard to get by on their current income. On the flip side, organisations may not be in a position to provide substantial pay rises to recognise employee effort, creating a perfect storm for financial stress. A possible consequence is that employees will leverage the ongoing war for talent and change employers to get a higher salary.

For those that do stay, financial stress might become evident through physical, emotional, and/or mental factors, such as increasing rates of absenteeism or falling productivity levels.

The C-Suite might point to the company’s benefits program as a solution, however our research reveals it often has a blind spot when it comes to effectiveness of these programs, and the level of stress in employees15.

Features of an Effective Financial Wellbeing Program

Critical to a financial wellbeing program’s effectiveness is recognising the diversity of spending attitudes and behaviours. Creating, or providing access to, a range of resources to suit various age groups and lifestyles is one step. There are some excellent online tools, and many EAP programs may also include budgetary advice in their menu of services.

It may be a matter of reviewing and adjusting your offer to ensure it is relevant to your workplace, and which may result in your employees having a better understanding of their own financial personality and what behavioural changes might help them.

Aon provides financial wellbeing programs to organisations globally across a range of industries and sectors. Our financial wellbeing team draws on Aon’s global insights from being a world leader in reward, benefits and wellbeing advice, and decades of devising effective employee engagement strategies.

Our experience has revealed a clear common denominator: the challenge of managing stress employees may have around finances. The current economic environment has elevated this risk, which may lead to retention and productivity issues and may make it harder to address the overall wellbeing of your people.

Clients who come to Aon for financial wellbeing programs receive tailored solutions for their individual challenges which may include the use of a unique financial wellbeing score that can identify cohorts of employees who are most in need of financial wellbeing support. Recognising that many People and Culture teams are already stretched, we are also able to provide a comprehensive suite of resources to assist with strategy implementation.

1 https://www.theguardian.com/business/article/2024/jun/07/australia-gdp-growth-figures-march-quarter-charts-cost-of-living

2 Reserve Bank of Australia. (2023). Statement on Monetary Policy - February 2023, Overview

3 Lifeline. (2024). What is financial stress?

4 Hong Kong Business, Hong Kong leads as the world's most expensive city

5 World Population Review

6 Demographia International Housing Affordability 2024

7 Business World, 4PH Program: Governments tool in addressing housing crisis

8 The India Employment Report 2024

9 Economic Times, Top IT Companies Cut Jobs

10 South China Morning Post, Jobseekers, employers in Hong Kong’s financial services sector have kicked off 2024 on cautious note

11 National Trades Unions Congress, Jobs Vacancies Report 2023

12 Phil Star, Job insecurity, climate change pose challenges in Philippines human development

13 Noypigeeks, Filipinos fear data leaks, job loss amid AI rise in 2024

14 Aon. (2023). Global Wellbeing Survey Report 2022-2023. Page 44

15 Fisher, J., & Silverglate, P. H. (2022). The C-suite's role in well-being