Member Options and Support – Looking at the Key Trends

Rebecca Peake, Senior Consultant, Aon

Rebecca Peake, Senior Consultant, Aon

Aon has recently completed its seventh annual Member Options and Support Survey, collating the views from nearly 300 UK defined benefit (DB) pension schemes.

In this article, we explore how schemes are supporting their members and the engagement that these initiatives are driving.

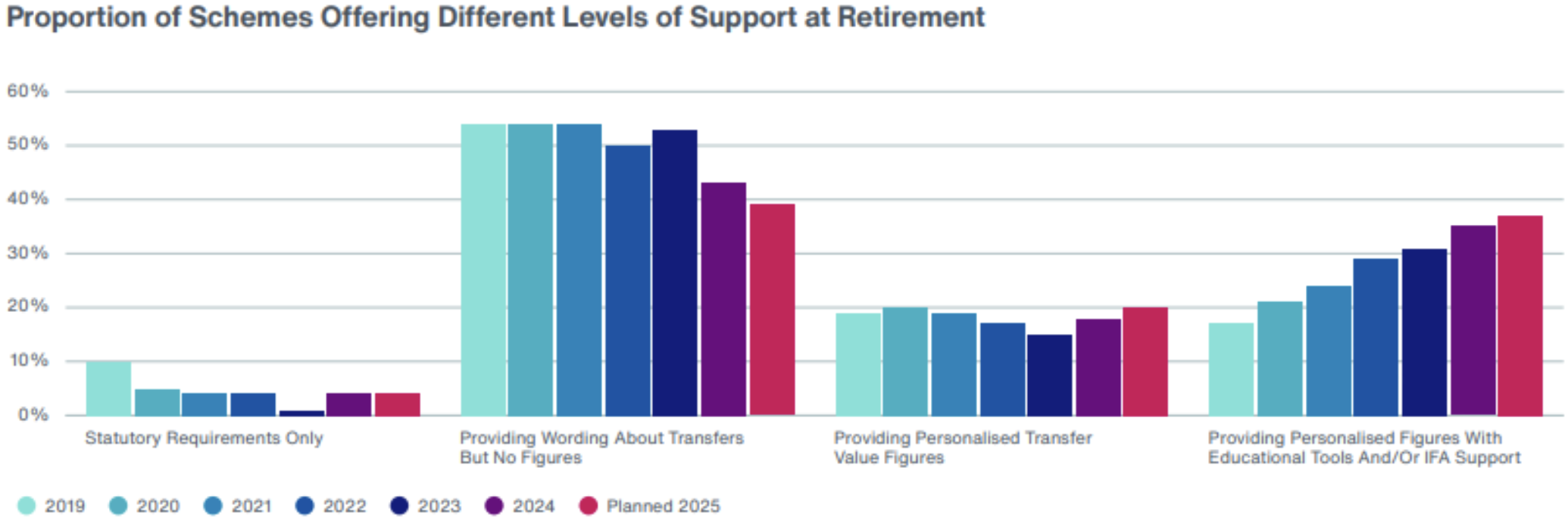

The trend for more support

Over one-third of schemes surveyed currently provide support to members through educational tools and / or independent financial advice. This has doubled in the last seven years, and that proportion is expected to increase to nearly 40 percent over the next year. This demonstrates that schemes – thankfully - continue to have the ‘member experience’ as a key part of their pension scheme agenda.

At the other end of the spectrum, we continue to see those schemes complying only with statutory requirements - with no mention of transfer options in retirement communications - are very much in the minority. Just under 5 percent of schemes surveyed fell within this category – but encouragingly this proportion has halved since 2019. There is also a continued downward trend for schemes providing just wording on the transfer option in retirement packs (personalised figures are provided on request).

The two groups of bars on the right-hand side below show the majority of schemes now provide personalised transfer value figures in retirement packs. Typically, these schemes that offer members personalised figures, also provide support to help members understand the information provided – with twice as many providing figures alongside access to educational tools and/or independent financial adviser (IFA) support compared to those providing figures alone. Feedback from trustees is that they feel more comfortable providing members with details of all the options, as long as additional support is also made available so that members can fully understand the information.

IFA support

Looking at IFA support in particular, the survey revealed that almost one-third of schemes provide IFA support, increasing from a quarter in our 2023 survey, with a further 4 percent planning on adding IFA support over the next year.

The financial choices to be made around retirement are among the most important an individual can make. Support from a qualified expert can help them make better decisions and be confident in their decision – regardless of whether individuals choose to retire from a scheme or transfer elsewhere.

Our survey results also continue to reveal a spectrum of approaches when it comes to offering IFA support to members. When IFA advice is provided, in the majority of cases (65 percent), it is paid for by the scheme trustee or corporate sponsor on behalf of the member which is a similar proportion to last year. But it does not have to be all or nothing. This year, 26 percent of schemes said they provide access to a preferred IFA or a panel of IFAs, but members are expected to meet the cost of advice themselves. The remaining 9 percent that provide members access to an IFA, do so on a subsidised basis.

When introducing IFA support for members, the scheme’s objectives are an important factor in considering whether to meet the costs in full or not. If a scheme is hoping to maximise engagement with the IFA, then providing paid-for financial advice is important. Alternatively, if the scheme’s objective is to instead make an IFA available to all members, a preferred IFA with members meeting the costs might be more appropriate. A preferred IFA, paid for by members, is still highly beneficial for members as it comes at a reduced cost (compared to using a self-sourced IFA) and a preferred IFA will have better knowledge of the scheme and streamlining the advice process with the administrator.

Flexibility for members

As well as an increasing number of schemes providing members access to education and support for planning their retirement, many schemes are also providing increased flexibility to members in how they can take their benefits at retirement. Aon’s 2023 Global Pension Risk Survey showed 30 percent of schemes now offer Pension Increase Exchange (PIE) or Bridging Pension Option (BPO) to members at retirement:

- PIE – offers members an opportunity to exchange some (or all) of their future annual pension increases for a larger one-off immediate increase in pension and lower (or no) pension increases in the future.

- BPO – enables members to take a higher pension from the scheme now and a lower pension after State Pension Age (SPA), smoothing their income so that their total income (from the scheme and the state) is broadly equal before and after their SPA. This option enables members to afford an earlier retirement and provides a solution for calls seen in the pensions press recently for people to be able to access their state pension earlier.

These options are popular with members, with our data showing that circa 50 percent of members are choosing to take one of these options where available. The popularity of these options being made available is continuing to increase, particularly with BPO where 70 percent more schemes offered a BPO in 2023 compared to 2022. We explored the trends of retirement options in more detail in our article earlier this year, which you can read here.

Increased support

The results of our survey show schemes are continuing to increase support for their members, and this is in line with what I am seeing with my clients – they want to do more for members. While being part of pension scheme objectives, it is also becoming easier to provide this additional support through better data, improved automation, and combining it with ‘must-do’ projects such as GMP equalisation, and to helping to prepare for the implementation of dashboards.

Over the coming years, I expect this trend to continue as more schemes at the lower end of the spectrum assess their position against other schemes and implementing dashboards which will require schemes to have more personalised figures immediately available for members.

If you would like to view our 2024 Market insights report in full, please do get in touch.

Aon Solutions UK Limited - a company registered in England and Wales under registration number 4396810 with its registered office at The Aon Centre, The Leadenhall Building, 122 Leadenhall Street, London EC3V 4AN.