Running on pension schemes – the member considerations

Gerrard Mckenna, Associate Partner

Gerrard Mckenna, Associate Partner

The economic events of the past two years have resulted in improved funding levels for many pension schemes - and pushing endgame planning high up the agendas of both trustees and sponsors.

The key question for many trustees and sponsors, is should you look to secure your scheme’s liabilities with an insurer or should you continue to run-on for the foreseeable future? Both transacting with an insurer and running on a scheme, have their benefits, but how does your endgame strategy impact the member experience? Why would a scheme choose to run-on and what are the key considerations they need to take into account?

To get a greater understanding on the endgame options on which schemes are focusing, Aon’s 2024 Member Options and Support survey asked participants about their long-term objectives.

- 54 percent of schemes indicated that they were targeting buy-in/buyout

- 20 percent of schemes had taken the decision to run-on

- 26 percent of schemes were yet to set their long-term target

Evolution of pension schemes

First, we need to look at the evolution of pension schemes, and why more schemes are offering members options and support at retirement.

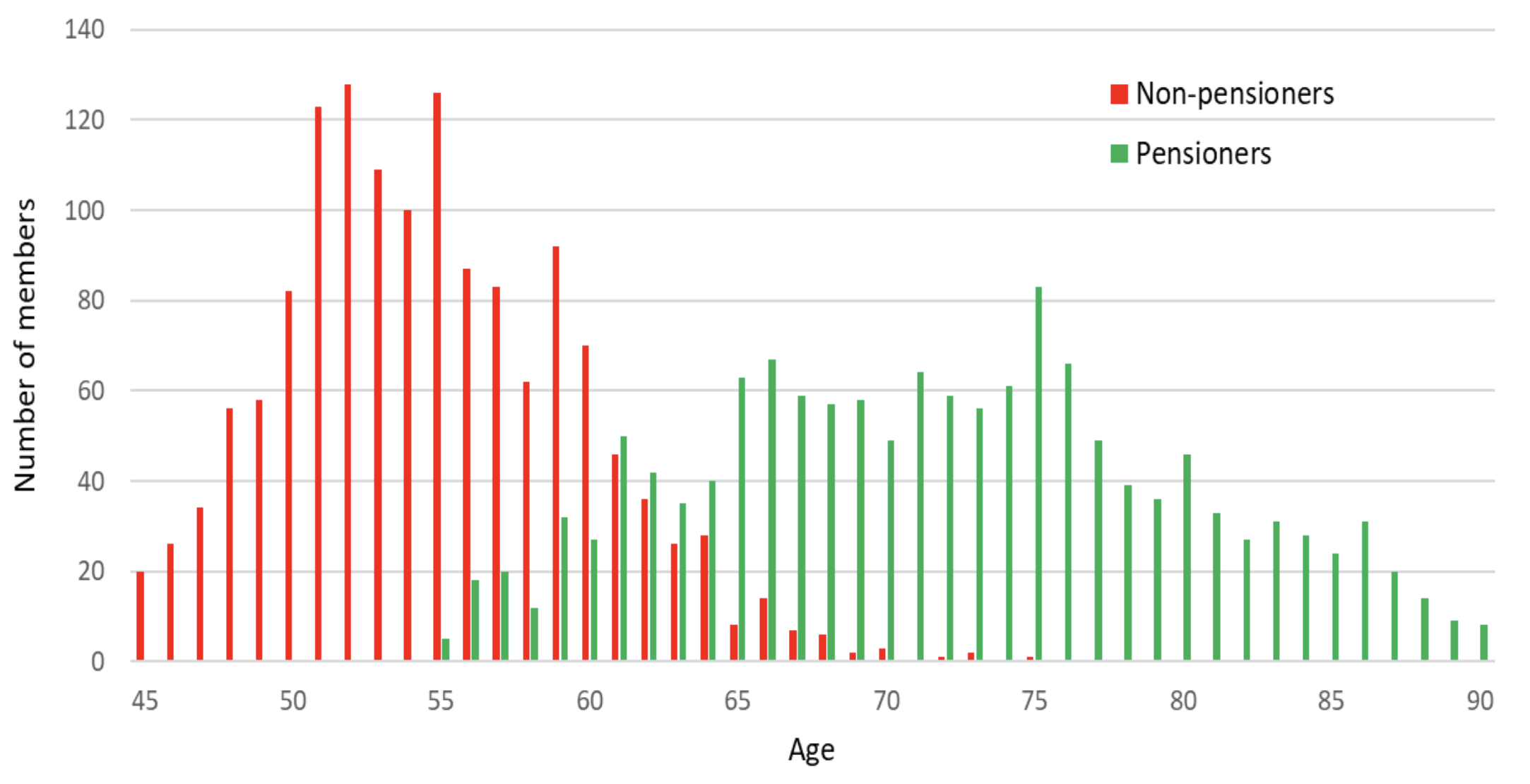

The expected rate of retirements over coming years is a key factor in why many schemes have put in place, or are looking to put in place, additional options and support at retirement. As a result, some schemes are electing to run-on until the majority of their non-pensioner members have retired.

Huge numbers of non-pensioner members in most DB schemes are expected to become pensioners over the next 5-10 years. The chart below demonstrates this evolution for a typical DB pension scheme, where the majority of the non-pensioner population is expected to hit retirement age over this period.

Understanding active run-on

Active run-on is the strategy of operating a well-funded pension scheme - with a strong covenant - with the explicit intent of building up surplus assets. The expectation is that the surplus can then benefit the key stakeholders of the scheme, the members, and the sponsor.

Active run-on strategies are being deployed both for short periods (say, 3-5 years with the expectation to buyout with an insurer after that period has elapsed) or as the endgame strategy for schemes running on indefinitely.

There are several ways that members can benefit from active run-on, including:

- Continued access to in-scheme options such as Pension Increase Exchange (PIE) and Bridging Pension Options (BPO)

- Retained access to support, for example, paid-for IFA advice

- Discretionary pension increases or benefit uplifts

It is important to note that the insurance market is evolving and insurers are building out their propositions and the support that members can receive post-retirement. For example, one insurer recently announced the provision of IFA support at-retirement (offered on a member pays basis) and other insurers are actively looking at offering similar support. Through early engagement with insurers, schemes may also be able to secure commitment to offering members BPO. All of this is good news for the member, although currently insurers do not typically offer the option of a PIE.

Other aspects that could negatively impact members after an insurance transaction (if currently offered and not insured) is discretionary pension increases or benefit uplifts. If exercised, discretionary pension increases can be a very immediate and valuable benefit for members. However, many schemes have a much broader range of discretions available to members, for example in relation to early retirement terms (in both normal and ill-health), payment of dependants’ pensions and sometimes simply long-standing administration practices that are not documented in the rules.

Another finding from our 2024 Member Options and Support Survey is that from the schemes offering IFA support, 65 percent of schemes offer this on a fully funded basis. This form of support is greatly valued by members to enable them to make informed retirement decisions. We mentioned that some insurers are looking at ways that they can offer members an IFA provision at retirement. This is likely to differ to the schemes’ selected IFA and although these costs are likely to be more favourable in comparison to high street costs, they are unlikely ever to be fully funded by the insurer.

Using active run-on to support DC members

There are also benefits to be had through accessing defined benefit (DB) surplus to support defined contribution (DC) provision. Where it is done correctly, there is real potential to achieve a win-win scenario for trustees, sponsors and (most importantly) members. We have already seen cases where DB surpluses are being used to benefit DC members. Examples include, increases being made to employer DC contribution levels - which has made a real difference in bridging the retirement income adequacy gap - and extending paid-for IFA support to DC members to support with their retirement decision-making.

For further information on considerations for implementing an active run-on strategy, please see here. If you would like to receive a full copy of our 2024 Member Options and Support Insights report, please do get in touch.

Aon Solutions UK Limited - a company registered in England and Wales under registration number 4396810 with its registered office at The Aon Centre, The Leadenhall Building, 122 Leadenhall Street, London EC3V 4AN.