DigiEco and Insurance Players – Winning the Game of Trust

As more and more consumers click for services and look to borrow rather than buy, the Digital Economy (DigiEco) will keep growing. DigiEco, essentially refers to businesses offering goods and services through mobile apps and other digital platforms that quickly match demand and supply.

Since, DigiEco platforms offer the ability to conduct trades anytime and anywhere from smartphones, companies also recognize the need for ‘ease’. There are numerous companies trying to create ‘ease’ in the market by creating on-demand services for everything - grocery delivery, ride sharing, home sharing are few such services.

While the internet economy has been moving ahead, the insurance market is not far behind on catching up with the trend. It is not always easy finding insurance options for the customers or owners of these companies that specialize in making business easy. As management-specific risks faced by DigiEco companies are only beginning to be understood, a report from Lloyd’s found that insurance plays a major role in bringing consumers on board, and that not all of them offer insurance.

Why do DigiEco companies need to offer insurance to consumers?

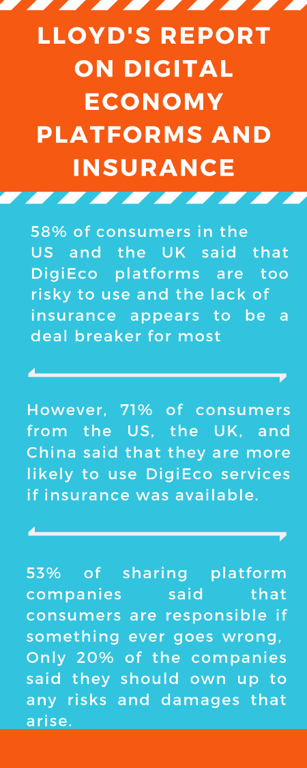

Many of the DigiEco platforms that participated in the survey – 78% of them – believe they will attract more customers if they offer insurance but were hesitant to take on the responsibilities that insurance implies.

On the consumer side, 53% said that sharing platforms are responsible in the event of risk, while 32% said that providers should be put on the notice when something goes wrong.

Insurance, hence, couldn’t be more important for companies like these. As soon as people are asked to share their time, co-share assets or rely on a platform for services, insurance is needed to deliver that trust factor.

What stops DigiEco companies from offering insurance?

Defining the risk

Traditional insurance coverages may not be readily applied to disruptive DigiEco models as assets are fragmented, owned and shared amongst users. Also, multi-party relationships among platforms, providers and consumers further draw questions around when and who is ultimately responsible for managing and mitigating risk.

Appetite of Carriers

There is a shortage of carriers that understand the space, the coverage(s) needed, what the expectations and the needs of these types of clients are. There is a wide gap between what is needed by the consumers and what is traditionally covered by the insurers.

Premium

Insuring such companies, their customers and new risks is not cheap and is certainly a barrier to getting the coverages needed. The rates are high, not much data is available, and claims are an unknown commodity.

Limited options and flexibility

Options like pay-as-you-go, pay-per-use are limited. Carriers are more comfortable dealing with traditional methods of payment. Flexibility is another critical factor missing in this evolving space, especially in terms of how policies are structured.

As people increasingly rely on DigiEco platforms to buy services or rent possessions from their peers, insurance cover is critical for the growth. To ensure protection for all parties, insurance players should meet the needs of this sector by offering solutions provided by platforms via transaction-embedded cover, or products purchased independently by DigiEco participants.

How Insurance can help DigiEco companies to develop better products for their customers?

When the DigiEco first came into being, appropriate insurance did not exist. The platforms relied solely on trust between users. While trust remains critical, the DigiEco comes with a unique set of risks which drive demand for new, innovative insurance solutions. It is here that Brokers’ expertise in creating successful alliances and partnerships in the insurance sector will be critical.

The evolution of the DigiEco brings Brokers’ to the limelight as the insurance industry will witness many changes as they move away from traditional coverages. The instant nature of the DigiEco means that personal and commercial lines will need to have cross over as policies become short-term. Brokers can look across different DigiEco models and start collecting data across different product classes, across different geographies and customer requirements and that gives the opportunity for fundamental change.

There are major opportunities for insurance companies who are willing to invest time and effort in the DigiEco space. Many organizations are already committing significant resources to the types of initiatives and will be first in line to market to the next generation of insurance customers. In short, there is power in alliances that can help support a new and endless combination of transactions leading to profitable growth. The key is to establish collaboration as a core competency, by being flexible and pursuing multiple strategies to create optionality.

Author -

Pankaj Puri

Vice President – Affinity