May 2019

By Adam Burn DipPFS, Principal – Employee Benefits

On April 6th this year the UK saw the final phase of the increase to automatic enrolment contributions, and there was a collective sigh of relief from Finance Directors, HR departments, employee representatives and pension advisors for its successful communication and implementation. However, it shouldn’t mask the fact that there is still a large issue regarding underfunding pensions which needs to be addressed.

When automatic enrolment was first proposed, the Pensions Commission issued a series of reports outlining their future vision for pension provision in the UK. The second report issued in November 2005 confirmed the desired contribution levels which finally came into force from April 2019.

Rather overlooked in the intervening years was the acknowledgement that these levels of increases are unlikely to provide a high level of retirement income, but merely help individuals improve their base level of income when combined with the state pension. The report highlights:

- The recommended minimum default level should be around 8% of earnings above the “Primary Threshold” – made up of 4% contributions from employees’ post-tax pay, 1% from tax relief / tax credit and 3% from matching compulsory employer contributions.

- The state pension is expected to deliver the median earner income equivalent to around 30% of median earnings in retirement.

- Based on “reasonable assumptions about rates of return and years of contribution” the default 8% contribution level will provide these median earners an additional pension, at point of retirement, of around 15% of their median earnings.

Critically, the report recommends that voluntary contributions on top of the default levels should be permitted to enable employees to contribute “in total about twice the default amount” in order to accumulate a pension approaching the two-thirds target replacement rate which many employees say is their target.

Do the financials add up?

In short, yes. The report refers to the median earner who – according to the latest figures (at 1st April 2018) from the Office of National Statistics (ONS) – earns £569pw, totalling £29,588 per year. The Commission then stated that under their proposals State Pension would deliver around 30% of this income in retirement. The 2019/20 full state pension is £168.60pw (£8,767.20 pa), which is actually 29.63% of this level of median earnings (assuming full entitlement is received). So far so good.

Assuming the “reasonable assumptions about rates of return and years of contributions” are accurate and the additional 15% of income will be achieved for the median earner, the result is that the average employee will have pension income from state pension age of around £13,205 per year – or roughly 45% of their pre-salary retirement.

But this raises two questions:

- Is this enough for individuals to live on in retirement?

- Does the average worker wish to work until state pension age?

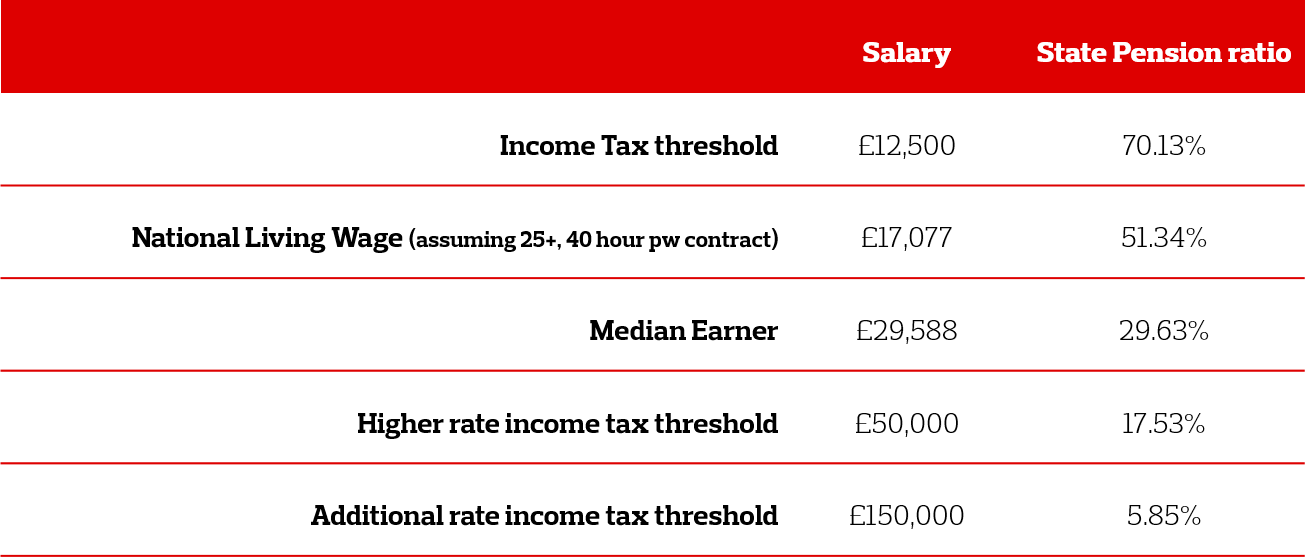

Of course, the fact that state pension will provide around 30% of pre-retirement salary is only applicable for the median earner. As the State Pension is a fixed amount it is a lower percentage of higher earners salaries and, conversely, a larger proportion for lower earners:

Therefore, whilst some lower earners may be relatively comfortable in retirement by contributing the minimum required percentages, higher earners may wish to consider paying higher pension contributions in percentage terms to compensate the shortfall.

What does this mean for employers?

If employees are unaware that paying statutory contributions may not provide a sustainable pension income, they might not be making alternative financial plans for retirement. If your employees cannot afford to retire, this could result in extensive employee dissatisfaction amongst both those unable to retire and any younger employees whose career progression is stalled by those in roles above them.

How can employers help?

Enhanced communication is key to help educate your employees that paying the statutory level of contributions is unlikely to provide sufficient pension income and they may need to commit higher payments to their pension in order to achieve the retirement income needed to fund their desired lifestyle. Additionally, facilitating regular expert reviews of pension funds and encouraging greater awareness around personal finance will help to give your employees the knowledge and tools to alleviate concerns around their retirement future. Although it may be a difficult conversation to have, providing guidance now may prevent disappointment in the years to come.

In conclusion it would seem that, in fact, the sighs of relief are potentially premature as the April 2019 increase to minimum statutory levels of contributions may prove not to be the end of the journey but merely a milestone along the road.

Aon provides expert support for companies looking to engage with employees about their pensions and benefits.

For more information or to discuss any of the issues outlined in this article, please get in touch by emailing us at letstalkbenefits@aon.co.uk or calling us on 0344 573 0033.

Aon UK Limited is authorised and regulated by the Financial Conduct Authority. Registered in England and Wales. Registered number: 00210725. Registered Office: The Aon Centre, The Leadenhall Building, 122 Leadenhall Street, London EC3V 4AN.