Pension Risk Transfer

What is Pension Risk Transfer?

As companies shift their retirement program focus to Defined Contribution (DC) offerings, plan sponsors are left with old Defined Benefit (DB) pension plans that can be volatile and difficult to manage. Pension risk transfer (PRT) is a way to shift those obligations off the company balance sheet and reduce risk by transferring the Plan’s obligation to an annuity provider. Plan sponsors can settle a subset of the population, usually retirees, in what is called a “lift-out” or the entire population through a plan termination.

What are the Benefits of PRT?

Historically, defined benefit pension plans have been used to recruit, retain and reward employees with pension benefits. However, as more defined benefit pension plans freeze accruals and close to new employees, they no longer provide the originally intended incentives. The pension plan liabilities can be volatile, costly and time-consuming to administer.

A pension risk transfer transaction can benefit an organization looking to de-risk and redirect resources to its primary business activities while upholding legacy obligations to plan participants. Choosing to initiate a PRT transaction may help organizations mitigate financial risks, including:

- Fluctuating interest rates

- Earnings volatility

- Participant longevity

- Investment return

- Administrative demands and expenses

773

In 2023, there were 773 PRT transactions totaling $45B in premium.

What are the Types of PRT Solutions?

The two primary types of PRT solutions in the U.S. are buy-outs and buy-ins. Buy-outs make up the majority of PRT transactions in the U.S.

What are Other Ways to De-Risk a Pension Plan?

Offering a lump sum window is another strategy to reduce the obligations of a pension plan. When a plan is terminating, plan sponsors usually offer a lump sum window to all terminated vested and active participants. Those who do not elect to take a lump sum will be included in the PRT annuity purchase at the end of the plan termination. Lump sum windows can also be offered while the plan is ongoing. This is typically offered to terminated vested participants, but it can also be offered to retirees and certain active participants.

Two

An annuity purchase comes in two options: a buy-out and a buy-in.

The most common ways to transfer risk are via:

-

Lump Sum Settlement

A lump sum settlement is a transaction where the plan pays a single lump sum to a participant (or designated IRA provider). The lump sum amount reflects the present value of all future expected benefit payments.

-

Annuity Buy-Out

An annuity buy-out is a transaction where an insurer provides an irrevocable commitment to directly make all future pension payments to plan participants until all obligations are satisfied. The pension plan no longer has any obligation to the participants.

-

Annuity Buy-In

An annuity buy-in is a transaction where an insurer provides a revocable commitment to fund future pension payments until all obligations are satisfied. The insurer pays the plan – not the participants. The buy-in is an asset of the pension plan and includes the option to convert to a buy-out.

How Can Aon Help with Pension Risk Transfer?

Managing risk and costs is an ever-present concern among corporate pension plan sponsors. Our goal at Aon is to help manage these risks and costs through innovative de-risking strategies, which include effective asset/liability management strategies. We collaborate with plan sponsors to develop strategies that address their specific risk and cost management objectives while bringing our market-leading expertise on pension de-risking.

-

Develop a Plan Specific Strategy

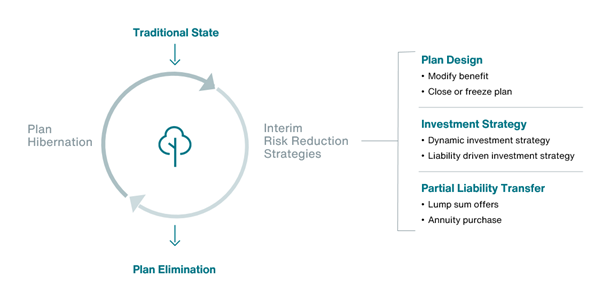

When developing an appropriate strategy, Aon utilizes a full suite of asset/liability management techniques ranging from interim risk reduction strategies (i.e., plan design review, investment strategy and liability transfer) to full pension plan termination. These strategies are developed to fit into a client’s overall risk management framework:

-

Analytics and Actionable Outcomes

Aon has a history of conducting robust feasibility analyses of de-risking and PRT opportunities. Our analysis focuses on providing plan sponsors with the information they need to enable them to assess the merits of acting. Aon focuses on education, financial outcomes, investment strategies, and a detailed review of data readiness.

-

Lump Sum Settlement

Aon’s Pension Administration team provides plan sponsors with project management expertise, participant communications custom-tailored to each plan notices, and internally processed participant elections.

-

Annuity Placement Leaders

Through our expertise and proven process, Aon is a leader in the PRT business. Since 2012, Aon has advised on over 488 annuity placements covering over $147 billion of premium. Aon has strong relationships with every annuity provider and a deep understanding of the due diligence requirements to assist in executing an annuity purchase.

Product / Service

Delegated Pension Manager

Report

2023/24 Global Pension Risk Surveys

The 2023/24 Aon DB Global Pension Risk Surveys findings represent the views of those managing defined benefit pension schemes. The survey looks at the different risks that pension funds are facing, including long-term targets, managing benefits and liabilities, investment strategy and local hot topics by country.

More Insights

-

Report 5 Min Read

U.S. Pension Risk Transfer Update -

Report 5 Min Read

U.S. Pension Risk Transfer 2024 Mid-Year Market Update -

Article 5 Min Read

Seizing Opportunity in a Booming Pension Risk Transfer Market -

Report 5 Min Read

Longevity, Socioeconomics and Pension Risk Transfers