With the Baby Boomer generation retiring, many employees are concerned about how they will pay for potential future

care. This is especially true of workers whose parents or older relatives are facing the prospect of paying for

long-term care (LTC) services. Since Baby Boomers are the largest generation, several issues have moved to the

forefront, including growing shortages as older nurses and care aides retire. Baby Boomers also have fewer children

to help take care of them, and those children have fewer resources with which to do so. With the average annual cost

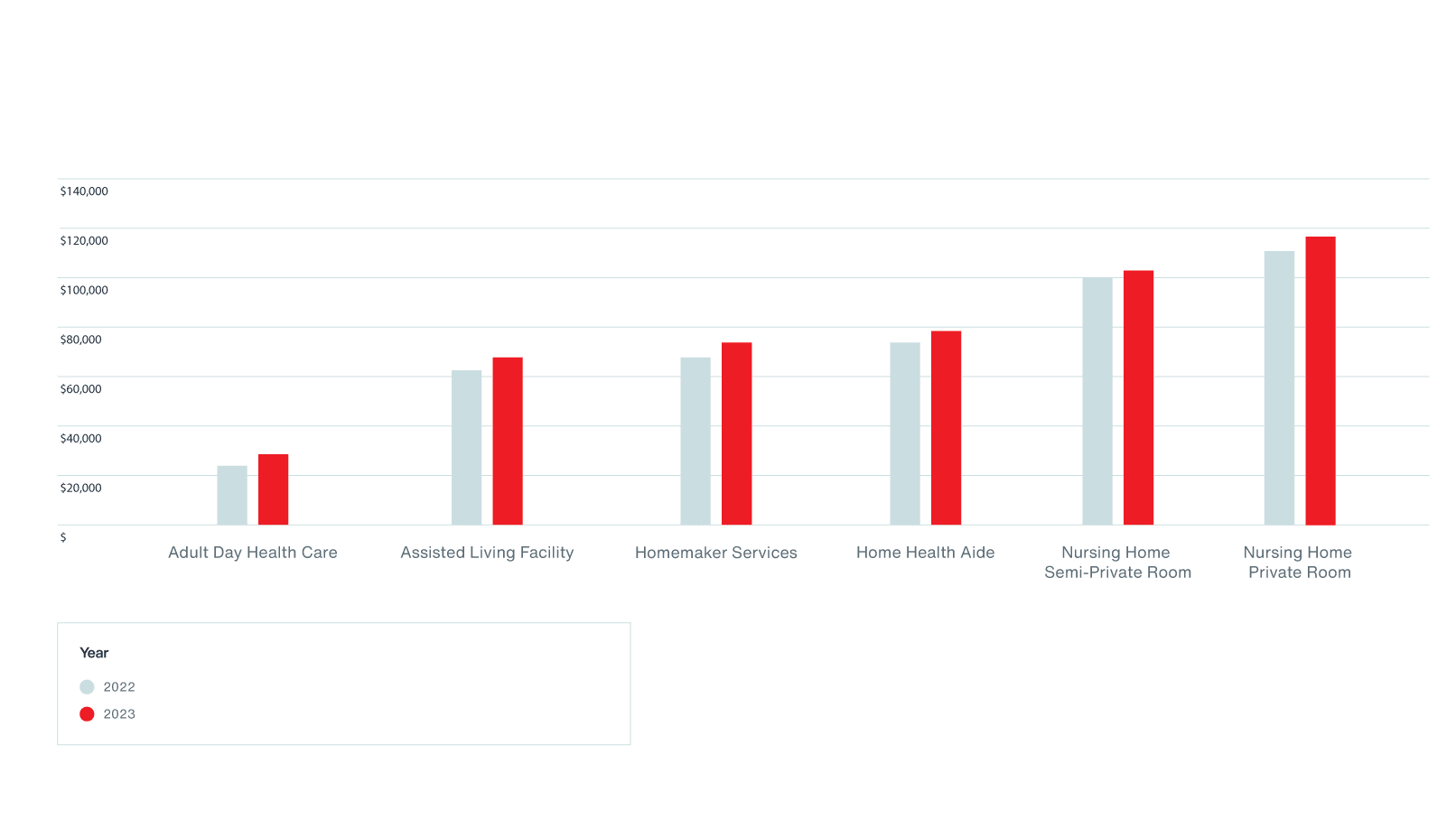

of a stay at a nursing home at well over $100,000,1 some have suggested that the “Great Wealth Transfer”

from Baby

Boomers to Generation X and Millennials will in large part be diminished.2

Contrary to what many may assume, Medicare doesn’t generally pay for LTC services. Rather, those costs are covered by

the individual, their families and by Medicaid. However, Medicaid’s strict asset limits, claw-back provisions and

limited options mean it is no panacea. That leaves seniors and their families on the hook for the cost of care. How

can employers help their employees plan for their future?