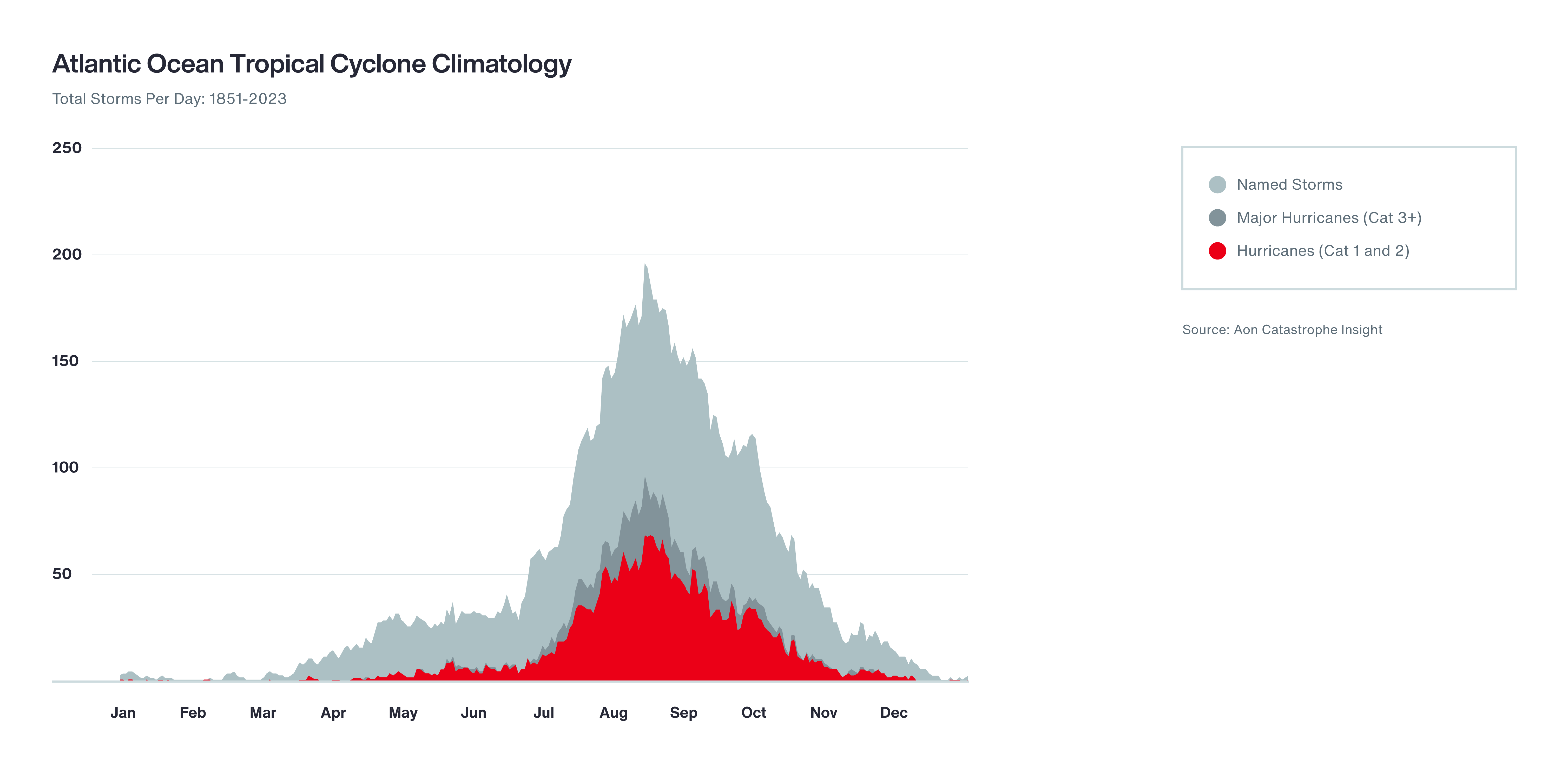

An expected mid-summer transition from El Niño to La Niña conditions, coupled with a warmer-than-usual tropical Atlantic, have tropical storm forecasters predicting an “extremely active” 2024 Atlantic Ocean hurricane season. Risk managers with occupancies in hurricane-prone areas are therefore encouraged to have a strong business resilience plan in place for an expected intense season.

category five strength of early-season Hurricane Beryl is a likely precursor to a “hyperactive season,” prompting hurricane researchers at Colorado State University (CSU) to slightly increase their July 2024 prediction with “above-normal”confidence.1 National Oceanic and Atmospheric Administration (NOAA) forecasters in May predicted an 85 percent chance of an above-normal season.2

Sea surface temperatures in the Atlantic Ocean are anticipated to maintain record-warm levels, creating the thermodynamic engine that enables hurricanes to intensify prior to making landfall. These rising temperatures can be attributed to the effects of climate change, but also El Niño itself, which tends to bring warm ocean waters back to the surface.3

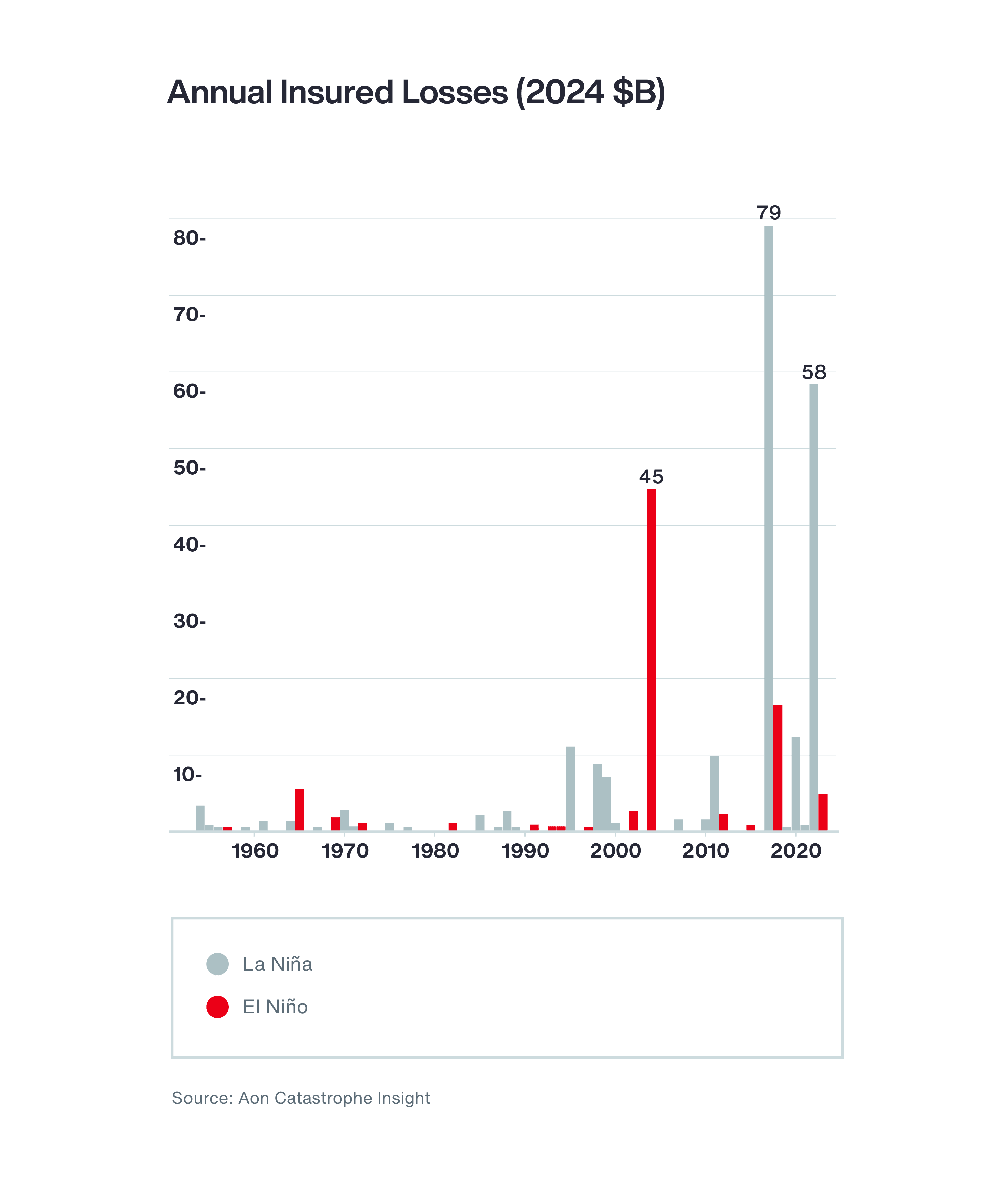

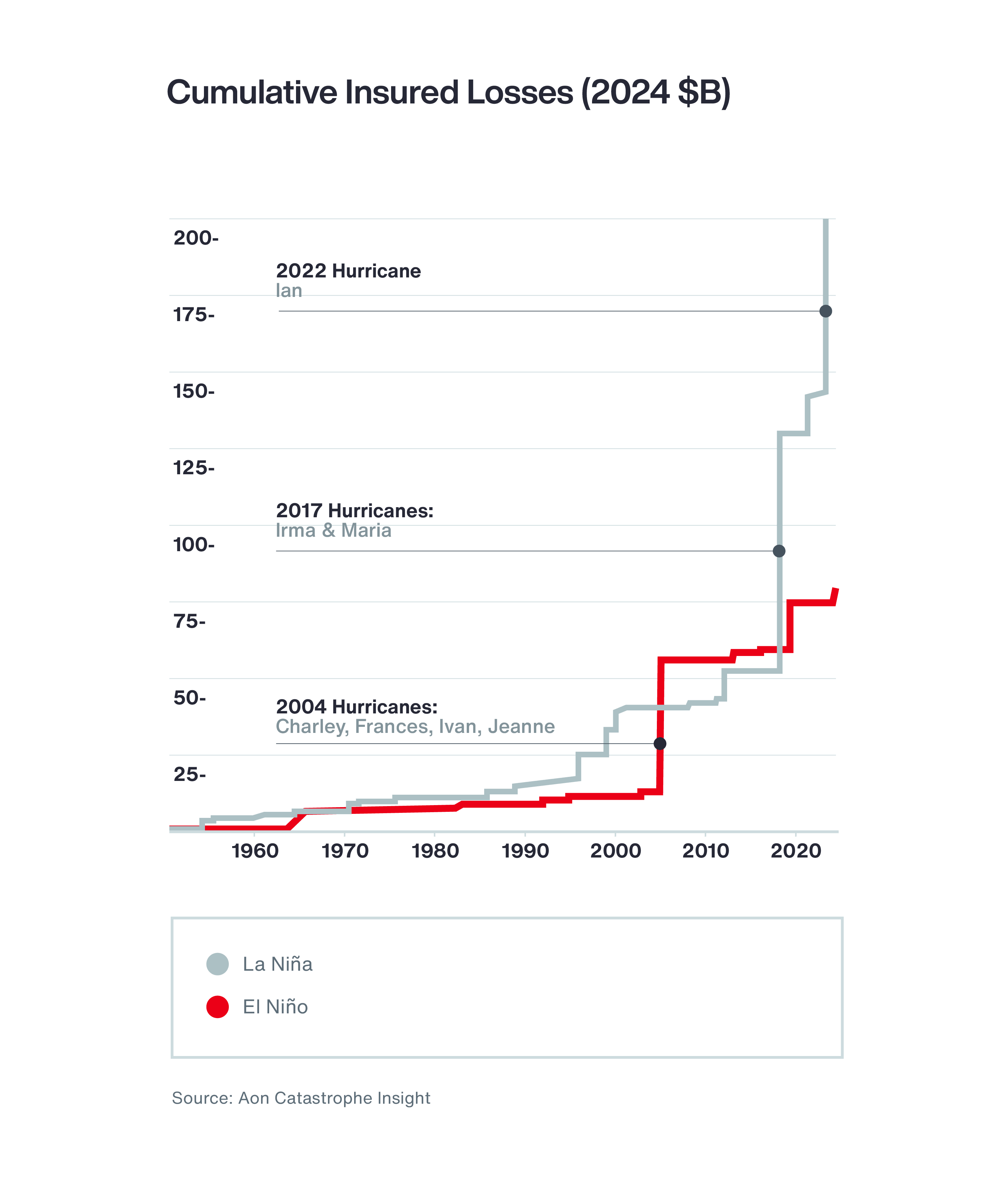

“The transition to a moderate or stronger La Niña is forecast to coincide with the peak of the North Atlantic hurricane season in late August through mid-September,” says Dan Hartung, managing director for Aon’s U.S. Reinsurance Catastrophe Analytics practice. “This could result in reduced wind shear across the main development region of the Atlantic Ocean, which is more favorable for tropical cyclone formation. La Niña also brings a greater chance of a stronger Bermuda High, which could potentially steer storms that do form further to the west, increasing the likelihood of U.S. impacts.”